Sale of Goods Act 1930

Till 1930,transactions relating to sale and purchase of goods were regulated by the Indian Contract Act,1872.In 1930,Sections 76 to 123 of the Indian Contract Act, 1872 were repealed and a separate Act called ‘The Indian Sale of Goods Act,1930 was passed.It came into force on 1st July,1930.With effect from 22nd September,1963,the word ‘Indian’was also removed.Now,the present Act is called’The sales of goods act,1930’. This Act extends to the whole of India except the State of Jammu and Kashmir.

Scope of the Act

The sale of Goods Act deals with ‘Sale of Goods Act,1930,’contract of sale of goods is a contract whereby the seller transfers or agrees to transfer the property in goods to the buyer for a price.” ‘Contract of sale’ is a generic term which includes both a sale as well as an agreement to sell.

Essential elements of Contract of sale

- Seller and buyer

There must be a seller as well as abuyer.’Buyer’ means a person who buys or agrees to buy goods[Section 2910].’Seller’ means a person who sells or agrees to sell goods [Section 29(13)].

2. Goods

There must be some goods.’Goods’ means every kind of movable property other than actionable claims and money includes stock and shares,growing crops,grass and things attached to or forming part of the land which are agreed to be severed before sale or under the contract of sale[Section 2(7)].

3. Transfer of property

Property means the general property in goods,and not merely a special property[Section 2(11)].General property in goods menas ownership of the goods.Dpecial property in goods menas possession of goods.Thus,there must be either a transfer of ownership of goods or an agreement to transfer the ownership of goods.The iwnership may transfer either immediately on completion of sale or sometime in future in agreement to sell.

4. Price

There must be a price.Price here means the money consideration for a slae of goods[Section 2(10)].When the consideration is only goods,it amounts to a ‘barter’ and not sale.When there is no consideration ,it amounts to gift and not sale.

5. Essential elements of a valid contract

In addition to the aforesaid specific essential elements,all the essential elements of a valid contract as specified under Section 10 of Indian Contract Act,1872 must also be present since a contract of sale is a special type of a contract.

Meaning and types of goods

Meaning of goods[Section 2(7)]

Goods means every kind of movable property other than actionable claims and money,and includes the following:

- Stock and share

- Growing crops,grass and thing attached to or forming part of the land which are agreed to be served before sale or under the Contract of sale.

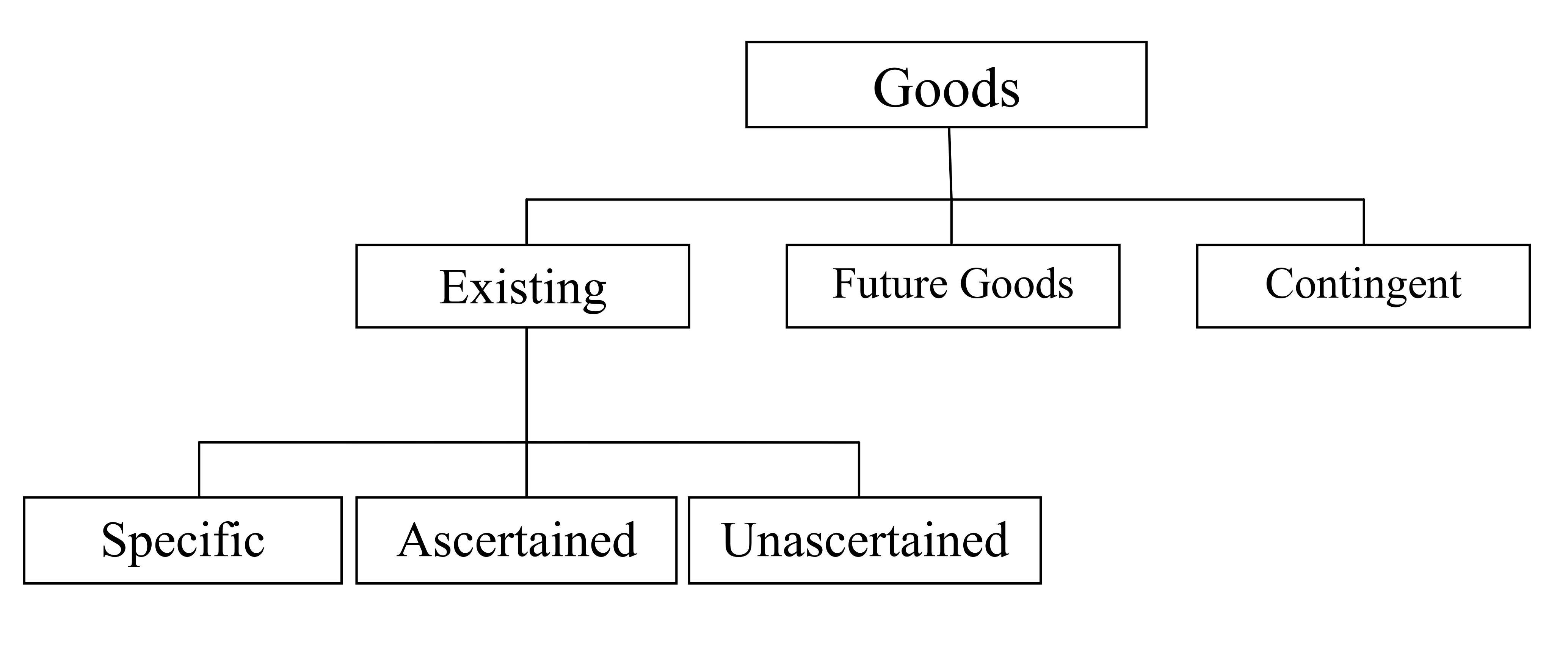

Types of Goods[Section 6]

- Existing Goods

Existing goods mean the goods which are either owned or possessed by the seller at the time of contract of sale.The existing goods may be specific or ascertained or unascertained as follows:

a) Specific Goods[Section 2(14)]:

These are the goods which are identified and agreed upon at the time when a contract of sale is made-For example,specified TV,VCR,Car,Ring.

b) Ascertained Goods:

Goods are said to be ascertained when out of a mass of unascertained goods,the quantity extracted for is identified and set aside for a given contract.Thus,when part of the goods lying in bulk are identified and earmarked for sale,such goods are termed as ascertained goods.

c) Unsanctioned Goods:

These are the goods which are not identified and agreed upon at the time when a contract of sale is made e.g. goods in stock or lying in lots.

2. Future Goods[Section 2(6)]

Future goods mean goods to be manufactured or produced or acquired by the seller after the making of the contract of sale.There can be an agreement to sell only.There can be no sale in respect of future goods because one cannot sell what he does not possess.

3. Contingent Goods [Section 6(2)]

These are the goods the acquisition of which by the seller depends upon a contingency which may or may not happen.